Introduction

As Christmas approaches, many UK businesses, from sole traders to limited companies, are planning to celebrate success, thank teams, and strengthen client relationships. Before booking venues or buying gifts, it is essential to understand how HMRC treats festive spending for tax purposes.

This guide explains which Christmas expenses are tax deductible for both self employed individuals and company directors, and where the rules differ. All information reflects HMRC guidance as of November 2025.

1. Staff Christmas Parties and Annual Events

Limited Companies

HMRC allows companies to host one annual staff event, such as a Christmas or summer party, tax free, if all the following apply:

a) The event is annual.

b) It is open to all employees, or all employees atone location.

c) The total cost does not exceed £150 per head(including VAT, travel and accommodation).

If all conditions are met, the expense is allowable for Corporation Tax, employees do not receive a taxable benefit in kind (BIK). Please note, if the event cost per head exceeds £150, the whole amount becomes taxable, not just the excess.

Input VAT can be reclaimed on costs for employees but not for clients or guests. Keeping attendance lists and invoices showing the per-headcalculation might be helpful.

Self-Employed

HMRC does not offer the same party exemption to sole traders or partners, since they are not classed as employees. However, if you have staff, you can apply the same £150 per head rule to those employees. If you work alone, a personal celebration is not deductible.

2. Employee Gifts and Christmas Bonuses

Trivial Benefits (for Companies).

Under the Trivial Benefits exemption (HMRCEIM21864), gifts can be tax-free if all of the following apply:

a) The cost ≤ £50 (incl. VAT).

b) It is not cash or a cash-equivalent voucher.

c) It is not a reward for work performance or part of the contract.

For directors of close companies, the total annual value is capped at £300 per tax year.

Self-Employed

Sole traders cannot apply the Trivial Benefits exemption, as it only applies to employees of limited companies. However, small non personal business gifts (e.g. a box of mince pies for clients) may still be allowable if they are wholly and exclusively for business purposes, modest, and not personal in nature.

Cash and Vouchers

Any cash or cash-equivalent vouchers are treated as earnings and must go through payroll for companies. For sole traders, they are not deductible as business expenses if for personal use or self-reward.

3. Office Decorations and Festive Extras

Limited companies: reasonable costs for decorating an office (tree, lights, ornaments) are allowable expenses. Self-employed (home office):decorations at home are not deductible, as they are deemed personal. Always keep receipts and ensure expenses are modest and business related.

4. Client Gifts and Entertaining

HMRC’s rules on client entertainment apply equally to both companies and self-employed:

- Entertaining clients or customers is not tax-deductible for Corporation Tax or Income Tax.

- VAT cannot be reclaimed.

Exception – Business Gifts. A business gift is allowable if it:

a) Costs less than £50,

b) Prominently displays your business branding (a branded mug or calendar), and

c) Is not food, drink, tobacco, or exchangeable for goods/services.

If clients attend your staff party, apportion the cost, only the employee portion remains deductible.

5. Sole Directors and One-Person Businesses

For a single director company with no staff, the following rules are applicable:

a) The £150 party exemption does not apply (since it’s not open to “all employees”).

b) You may still claim Trivial Benefits up to £300 per year.

c) Any Christmas bonus must be processed through PAYE.

For self-employed individuals, personal festive spending is never deductible, but modest client gifts (under £50 with branding) can still be claimed.

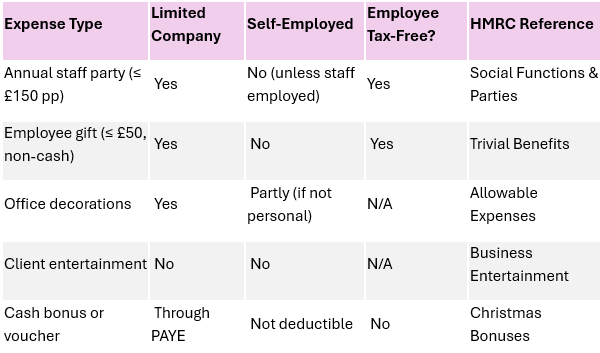

6. Summary Table

7. Record Keeping Checklist

To stay compliant and support your claims:

a) Keep receipts, invoices, and attendee lists.

b) Record the cost per head for any events.

c) Separate staff and client costs.

d) Maintain a gift register for Trivial Benefits.

e) Keep evidence for potential HMRC review.

Conclusion

Christmas is the perfect time to celebrate your team’s effort or thank loyal clients, and, with good planning, you can staytax-efficient too. Know the HMRC limits, document every cost, and apply the rules consistently.

If you are unsure whether your festive expenses qualify for tax relief, speak with your Chartered Accountant for tailored advice (info@schoolgateaccounts.co.uk, +44 7825 308400).

Disclaimer

This article provides general information as of 6 November2025 and should not be relied upon as professional advice. Always seek guidance from a qualified Chartered Management Accountants regarding your specific circumstances.